This book is an intellectual history of economics with a focus on a handful of names: Karl Marx, Alfred Marshall, Beatrice Webb, Irving Fisher, Joseph Schumpeter, John Maynard Keynes, Friedrich Hayek, Joan Robinson, Milton Friedman, Paul Samuelson, and Amartya Sen.

As you can see, those choices are idiosyncratic. Most modern economists would not include Marx, Webb, and Robinson since they are off in the dead end of Marxist "economics". But for me they are part of the spice of this book. This isn't a text to teach you economics. It is really more of a history of personalities and circumstances. The stories are delightful. The sketches of economics are thin gruel, so don't come here to understand economic theory. Come to savour history, personalities, and ideas.

What I found delightful is that the book reinforced my prejudices. Economics is not a "science". It is a liberal art with the pretension of science through its mathematicization of its arguments. The formalism doesn't make the models and arguments any more right. They do provide a bit more formal clarity but they also lead to obscurantism with dithering over details and ridiculous "simplifying" assumptions. I had a mathematician as a friend who made this point by arguing about cows by first stating "consider a sphere". Yep... mathematics does some wonderful leaps in simplification to make the mathematics "tractable".

Here are some snippets to give you a feel for the writing style:

Before resuming his journey north to the Scottish highlands, Alfred Marshall, a twenty-four-year-old mathematician and fellow of St. Hohn's College in Cambridge, spent hours walking through factory districts and the surrounding slums "looking into the faces of the poorest people." He was debating whether to make German philosophy or Austrian psychology his life's work. These were his first steps away from metaphysics and the beginning of a dogged pursuit of social reality. He later said that these walks forced him to consider the "justification of existing conditions of society."

In Manchester, Marshall found the smoky brown sky, muddy brown streets, and long piles of warehouses, cavernous mills, and insalubrious tenements -- all within a few hundred yards of glittering shops, gracious parks, and grand hotels -- that novels such as Elizabeth Gaskell's North and South had led him to expect. In the narrow backstreets he encountered sallow, undersized men and stunted, pale factory girls with thin shawls and hair flecked with wisps of cotton. The sight of "so much want" amid "so much wealth" prompted Marshall to ask whether the existence of a proletariat was indeed a "necessity of nature," as he had been taught to believe. "Why not make every man a gentleman?" he asked himself.

...

He took great pains to demolish Socialists' claim that but for oppression by the rich, the poor could live in "absolute luxury." England's annual income totaled about £900 million, he told the women. The wages paid to manual workers amounted to a total of £400 million. Most of the remaining £500 million, Marshall pointed out, represented the wages of workers who did not belong to the so-called working classes: semiskilled and skilled workers, government officials and military, professionals, and managers. In fact, an absolutely equal division of Britain's annual income would provide less than £37 per capita. Reducing poverty required expanding output and increasing efficiency; in other words, economic growth.

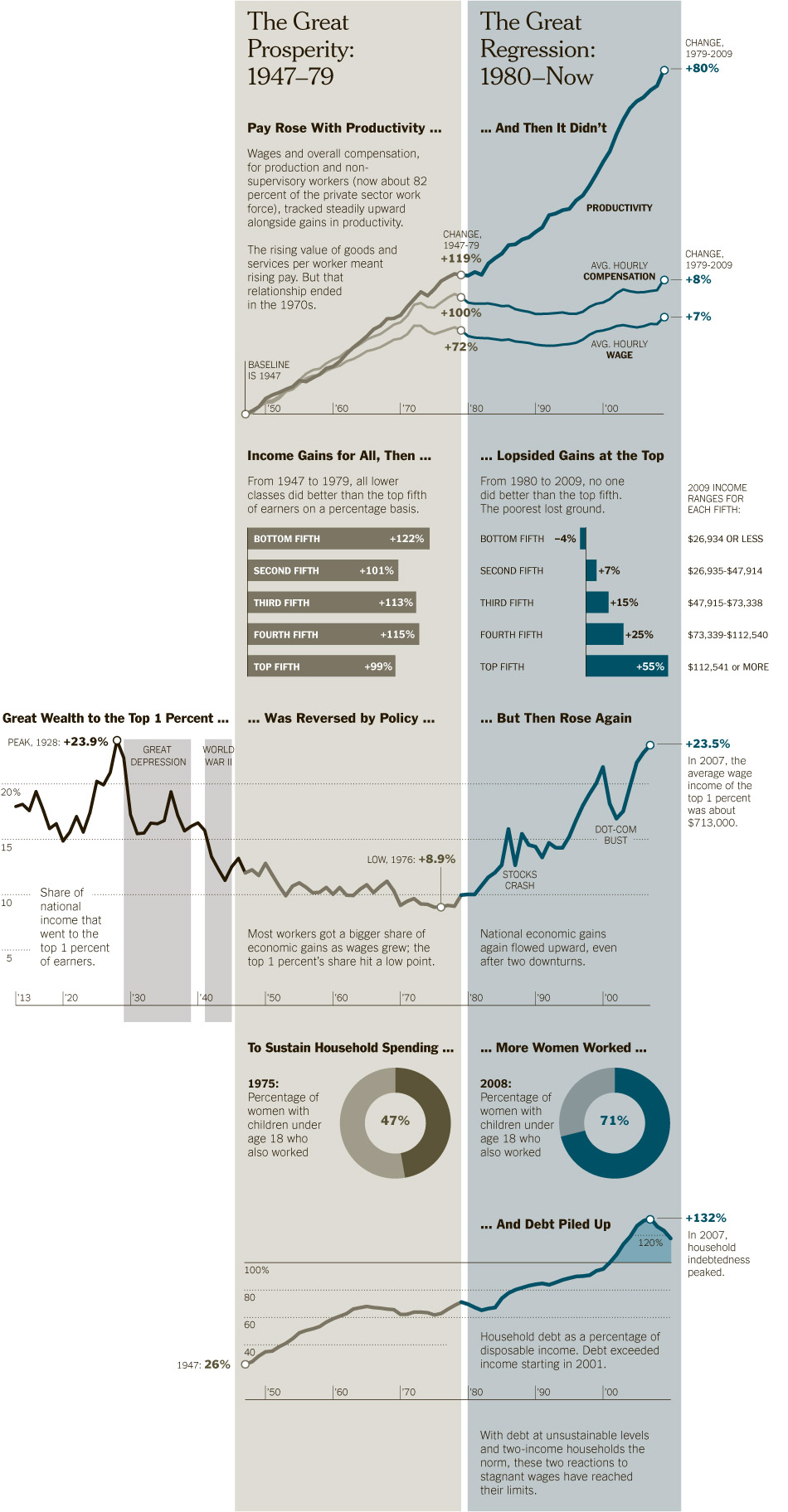

One of the points that Nasar makes is that modern societies organized around liberal economic principles has unleashed productivity and wealth. But as I read the above I keep picturing the billionaire tycoons on Wall Street and the masses in the street with their

Occupy Wall Street protests. Sure there has been progress, but the economic injustice is still just as bad. The greed and indifference is there which exacerbates the pain. The fact that the billionaires can buy the politicians means that nothing will ever change. The fact that the rich are pushing to cut education and social services while cutting taxes on the rich as their "solution" to the current Lesser Depression is very depressing.

Sylvia Nasar's story points out that the same humbug and foot-dragging that blocked a real solution to the Great Depression was very, very similar to the humbug and foot-dragging of today:

Despite his financial straits, damaged reputation, and advancing age, the sixty-five-year-old Fisher seemed more energized than depressed by the economic calamity. In 1932 he published an extraordinary number of scientific papers and newspaper pieces. He bombarded the Hoover administration and the Federal Reserve with advice and organized other economists to do the same. His chief objective was to convince President Hoover to take the United States off the gold standard, if not de jure then de facto by having the Federal Reserve do nothing to prevent the foreign exchange value of the dollar from falling. He met with the bankers at the Federal Reserve to urge them to adopt an aggressive program to buy bonds from the banks and the public in order to pump money into the banking system. To his frustration, the "Federal Reserve men thought it would be 'safer' if they waited!" as he later complained. "That waiting, in my opinion, cost the country the major part of the depression."

In January 1932, Fisher attended a second meeting of monetary experts at the University of Chicago. This time, he organized a telegram urging the president to permit the federal budget deficit to rise, pump reserves into the crippled banking system, slash tariffs, and cancel inter-allied debts. Thirty-two prominent economists from Chicago, Wisconsin, and Harvard universities signed the statement, in which Fisher pointed out that Sweden, Japan, and Britain were recovering after going off gold the previous year. The signatories reflected the extent to which Fisher and Keynes's view of the crisis with its emphasis on its global nature, monetary causes, forecasts of its future course, and the need for concerted monetary intervention had gained adherents. On the other hand, theirs was still a minority view.

Sadly, today Obama ignores neo-Keynesian solutions. He shows himself to be uneducated about economics and has surrounded himself with the same fanatical deregulation libertarian economists who created this Lesser Depression. There has been absolutely no progress in economic "science" in 80 years. The same humbug and "morality play" rationalizing goes on to protect bondholders at the expense of the 25 million unemployed, the 10 million who are losing their homes, the youth who have given up on education because it is too expensive, and those nearing retirement who are desperate because their savings are exhausted. It is a social disaster, but Obama is acting like a modern Hoover and the 2012 Republican presidential candidates would make Hoover look like a bleeding-heart liberal. Tragic.

Sylvia Nasar traces out Keynes' thinking:

As the Great Depression dragged on, Keynes's faith in the effectiveness of monetary policy ebbed further. By the time A Treatise on Money appeared, he was beginning to pose a theory of the causes of unemployment. Cambridge undergraduates were his first audience. The nub of the new theory was that, as he put it in an article published in the American Economic Review in December 1933, "circumstances can arise, and have recently arisen, when neither control of the short-rate of interest nor control of the long-rate will be effective, with the result that direct stimulation of investment by government is a necessary means."

In a severe depression, prices fell even faster than interest rates. So reductions in nominal rates did not prevent real rates from climbing. Once nominal rates fell to zero, there was nothing further that the central bank could do to make borrowing cheaper or to ease debt burdens and thus to end the depression -- with incalculable political consequences, what Keynes called The Liquidity Trap. As he had once observed, "The inability of the interest rate to fall has brought down empires." Once monetary policy was rendered ineffectual, the only option for shoring up demand was getting money into the hands of those who could spend it.

...

As Herbert Stein, the economist, pointed out, Keynes asked a very different question from the one posed by Hayek and Schumpeter. In explaining depressions, in terms of the preceding booms, the Austrians were trying to figure out how the economy had gotten there. Keynes was less interested in the genesis of slumps than in the more basic puzzle of how high unemployment and slack capacity could persist for long in a free market economy with unrestricted competition.

...

Thus what made the General Theory so radical was Keynes' proof that it was possible for a free market economy to settle into states in which workers and machines remained idle for prolonged periods of time -- that there were depressions that, unlike the garden-variety ones, were not brief and didn't end of their own accord as a result of falling prices and interest rates, or, at an extreme, that free market economies tended naturally to stagnate even when there were idle workers and machines available. In such depressions, unfreezing credit flows through monetary policy didn't provide a sufficient stimulus, because even zero-percent interest rates could not tempt businesses to borrow while prices were falling and there was [no] reason to think that demand would recover. The only way to revive business confidence and get the private sector spending again was by cutting taxes and letting businesses and individuals keep more of their income so that they could spend it. Or, better yet, having the government spend more money directly, since that would guarantee that 100 percent of it would be spent rather than saved. If the private sector couldn't or wouldn't spend, then the government had to do it. For Keynes, the government had to be prepared to act as the spender of last resort, just as the central bank acted as the lender of last resort.

This is the same intellectual landscape that has policy makers hung up today. Bernanke and the Federal Reserve have been too timid in using monetary policy and now the only tool left is fiscal stimulus, but you have right wing nuts screaming about "inflation!" and "debt!". Obama is too timid to properly stimulate the economy and instead falls into the trap of Hoover and

FDR in 1937 of worrying about deficits and debts. They ignore the ruined lives and the lost production that can never be retrieved while the country stays mired in a depression. The arguments of 80 years ago are lost to policy makers today because they are illiterate about history and economics. Oh, and they are blinded by their ideology, an ideology bought and paid for by the billionaire ultra-rich who are quite happy to leave the system just as it is, a system that has let them exploit it for billions in personal gain. This is a tragedy for the bottom 99%. The top 1% are laughing, but the bottom 1% are paying in ruined lives... and they will also pay through taxes to cover the lost monies and even provide the billionaire bonuses for the frauds and cheats who created the mess. Sorrows heaped on woes, and smothered with injustice.

This is a good read and it is highly relevant. This book will give you useful background to understand the economic arguments of today and the tragedy that today is a maddening repeat of the 1930s.

{kind=link}

{kind=link}

{kind=link}